Market price on the date of suggestion – 830Rs.

Birla Corporation (BCL), a flagship company of the MP Birla group is engaged in the business of manufacturing and sales of cement. The company is also into sales of Jute, PVC goods and automotive trim parts.

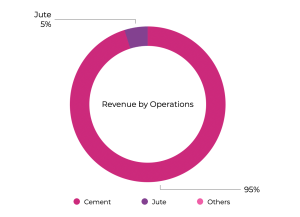

The company originally incorporated in Aug 1919 as Birla Jute Manufacturing Company was renamed in 1998 to reflect its diversified operations. As on date, cement is the largest contributor to the company’s revenue (over 90%) with the remaining coming from jute and other products.

Business Segments

Cement

The Cement Division of Birla Corporation Limited manufactures varieties of cement, including Ordinary Portland Portland_Cement (OPC), 43 & 53 grades, fly ash-based Portland Pozzolana Cement (PPC), Portland Slag Cement (PSC), low- alkali Portland cement and Sulphate Resistant Cement (SRC).

About Darkhorsestocks – DARKHORSESTOCKS are those which are fundamentally strong, have good growth potential and very few people know about. We suggest only one such idea every week on Sunday. So far majority of those stocks have delivered above 35% returns in over a year with some of them giving exceptional returns. For Whatsapp Updates Click here.https://wa.me/917874999975?text=Subscribe

During the year 1996, a joint venture company Birla Redland Ready mix Ltd.’ was incorporated with Redland PLC, UK to set up facilities for manufacture of ready mix cement concrete in India. Effective from 31st March of the year 1997, the name was again changed from Birla Jute & Industries Limited to Birla Corp Limited. In 1998, the company had sets up a fly ash-based cement-grinding unit at Rae Bareilly in Uttar Pradesh. The name was again changed from Birla Corp Limited to the present name Birla Corporation Limited in 27th October 1998.

Birla Corporation launched premium quality Portland Slag Cement (PSC) brand, Birla Samrat UNIQUE, in Eastern India in 2011.

BCL on a standalone basis has seven cement plants spread across four states of Rajasthan, Uttar Pradesh, Madhya Pradesh, and West Bengal with an aggregate installed cement capacity of 10.00 MTPA per annum.

In August 2016, BCL successfully acquired 100% equity stake in Reliance Cement Company (RCCPL) to expand its cement business. At present, BCL along with RCCPL have a group installed cement capacity of 15.58 MTPA.

Keeping in view the rapid growth in infrastructure and projects, the company launched new-age cement brands, M P Birla Cement CONCRECEM (OPC 43 & 53 grades) and MULTICEM (fly ash-based PPC) in March 2017. These products are particularly suitable for large commercial, industrial, infrastructural and real estate projects. MULTICEM is a BIS-certified PPC cement, specially engineered for infrastructural development. It is manufactured using the latest cement manufacturing technology and ultra-modern techniques.

Company’s MP Birla Cement ‘master brand’ was forcefully established in the market with a powerful multimedia campaign, ‘Cement se Ghar tak’, and a new brand architecture was developed for the product brands.This led to enlarging the footprint of the MP Birla heritage brands (Samrat and Chetak) into the high growth markets of Madhya Pradesh, Maharashtra (Vidarbha) and Uttar Pradesh.

The company has strong presence in Central (Madhya Pradesh) and Northern regions (Uttar Pradesh & Rajasthan) of the country with other key markets of the company being Haryana, Bihar, Bengal, Delhi, Gujarat and Maharashtra. BCL sells cement under various well established brands, prominent being MP Birla Perfect Plus, MP Birla Unique, MP Birla Samrat, MP Birla Ultimate, MP Birla Ultimate Ultra, MP Birla Chetak, MP Birla Concrecem, MP Birla Multicem, and MP Birla PSC Samrat.

The company has a strong network of 1250 marketing staff, 300 sales promoters and more than 10000 dealers (both BCL and RCCPL). On a combined basis, the plants cover an average radius of approximately 350 kms

Jute

The Jute Division of the company manufacturing more than 120 tonnes of a variety of jute products in Birla Jute Mill. The product range comprises of almost every major application of jute – the most versatile, eco-friendly, biodegradable fibre available, Jute- durable, natural and anti-static.

The Jute business of the company alike the industry peers is dependent on government orders (for pro procurement of food grains under the Jute Packaging Materials Act) and currently government orders currently account for about 70 per cent of installed production capacity. Though the company focus on exports of value added products it still accounts just about 12% of overall sales in FY20.

Aggressive Steps taken

The company leveraged its strong brand to get into allied construction products such as Wall Putty and construction chemicals. Wall putty and construction chemicals launched during the year under the Perfect Plus franchise in select markets have been received well and have even started to make a modest contribution to the Company’s profitability. The Company plans to scale up the business and expand profitability by adding new products to the range and by optimising the supply chain.

One of the key specialities of us at darkhorsestocks is that we try to present the stocks which are not very common or hardly few people actually know about. Most of the darkhorsestocks ideas are not covered by any of the brokerages or research house by presenting research reports .

BCL’s key markets witnessed strong recovery in cement demand Construction sector though in general is still crippled by COVID 19 pandemic that is largely pronounced in major metros.

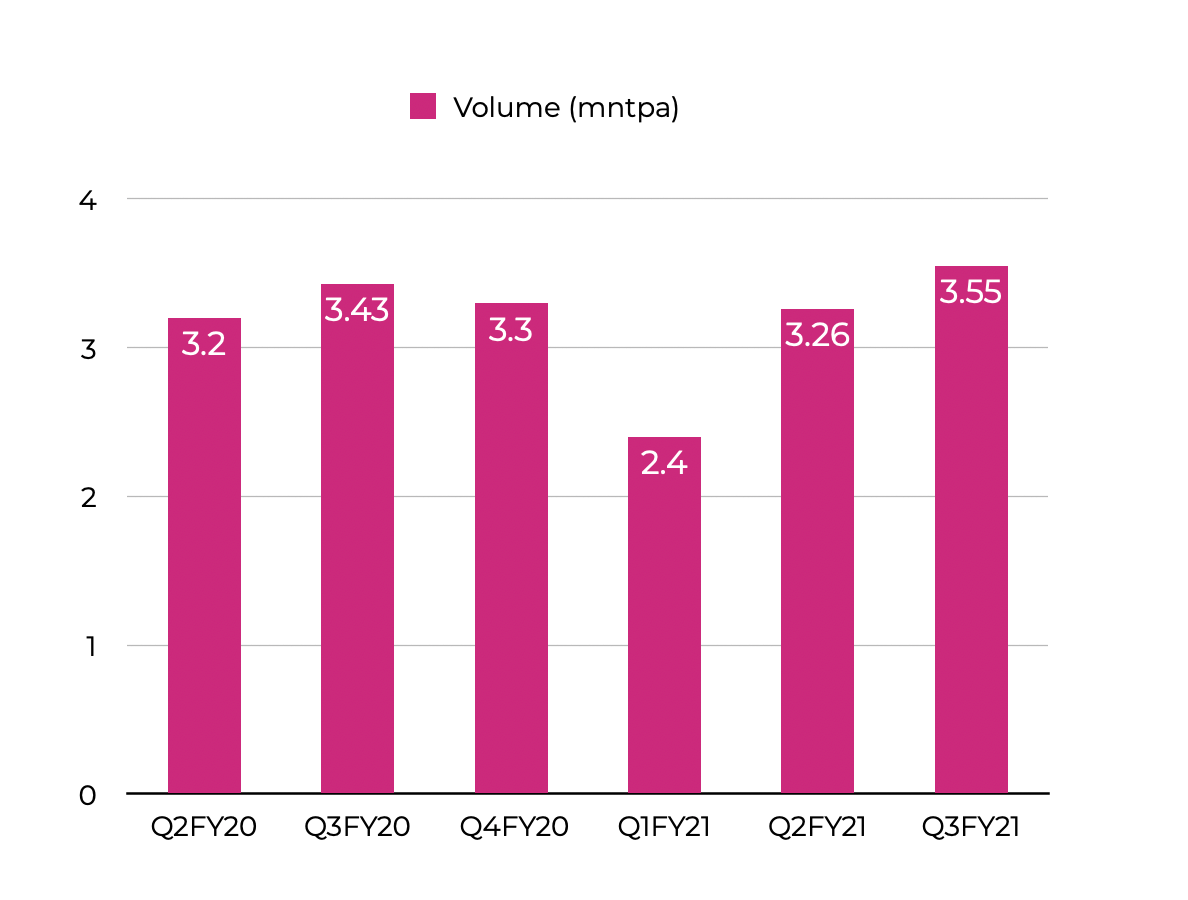

In Q2FY21 the sales volume of the company grew 2% to 3.26 million tonnes as the cement demand in BCL’s key markets such as Uttar Pradesh, Madhya Pradesh and Bihar was better than expected largely on account of demand for rural housing and government spending on rural infrastructure.

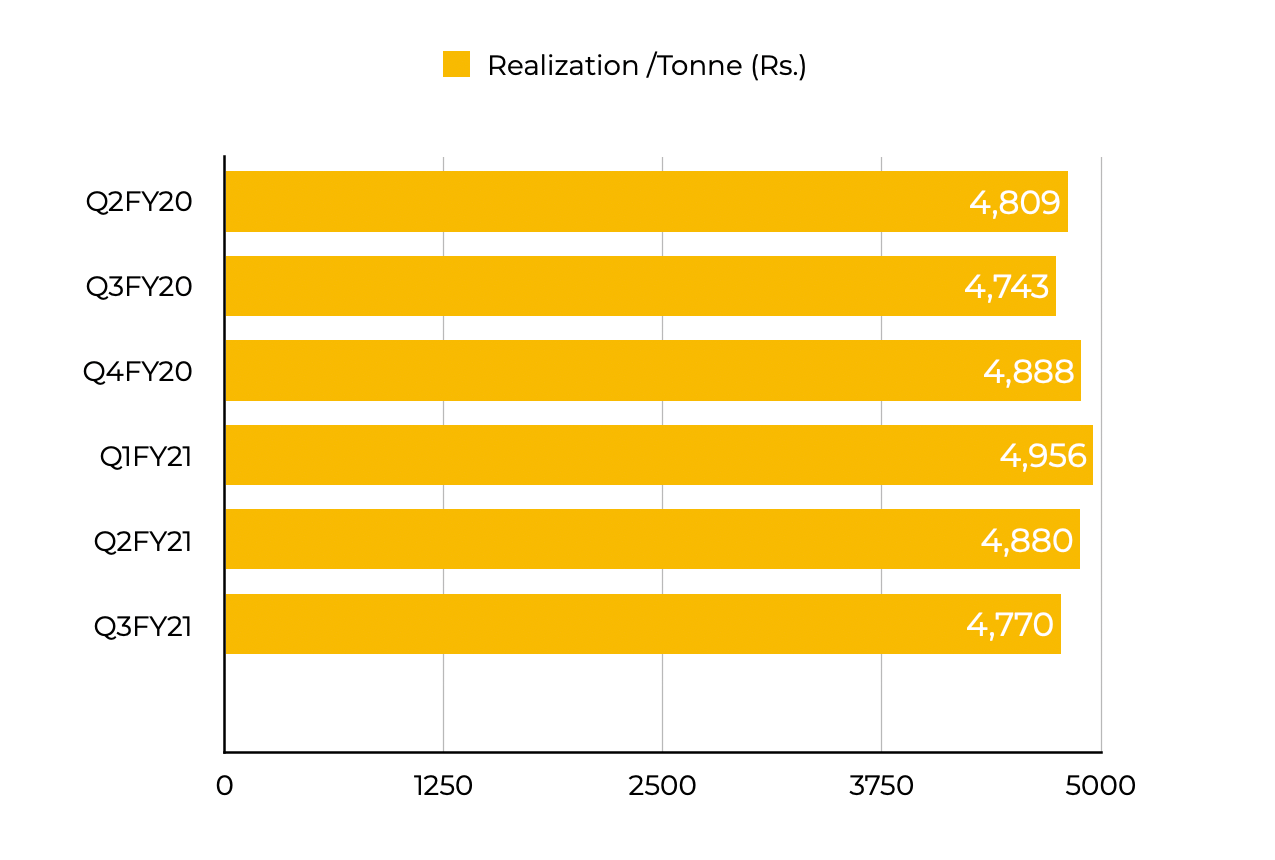

With sustained increase in both share of premium cement and blended cement share, the realisation in H1FY21 was up by 0.2% to Rs 4881/ton and up 1.3% to Rs 4862 in Q2FY21.

The company continue to focus on offering high quality products to customers and makes sustained investment brands and distribution assets to make it possible. As result of this the share of premium cement by volume within the trade segment rose from 37% in 2018-19 to 41% in FY2020. This has further increased to 46% in H1FY21 (up from 38% in H1FY20). The share of premium cement was at a high of 48% in Q2FY21.

The management expects better demand environment to prevail for the rest of the year. Share of premium products on steady rise and to facilitate higher profitability The company in FY20 managed to increase the price realisation up by 5.7% to Rs 4811/ton despite muted market conditions.

The share of high yielding blended cement also on rise from 89% in FY19 to 93% in FY20 and further to 93.8% in H1FY21. The EBITDA/ton for H1FY21 was up by 8% to Rs 1080 and that for Q2FY21 was up by 20.8% to Rs 1154.

Expansion

The company is in agressive expansion mode with its Greenfield Maharashtra plant to get commissioned by Sep 2021 , expansion of its Kiln capacity at its Chanderia unit by 400000 tons and with 40 MW captive power plant and 10.6 MW Waste Heat Recovery Systems at an estimated cost of Rs 2450 crore.

With overall cement capacity utilisation of the company in FY20 stand at about 91% (on a monsoon quarter ended Sep 2020 (Q2FY21) the utilisation stood at 84% compared to 83% in Q2FY20) additional capacity coming on stream will help the company to address capacity constraint for growth.

Going Forward

The management is confident of achieving its target of reaching 25 million tons of capacity by 2025, which translates into 62% growth in capacity over the next 4 years.

Financials

For the quarter ended Sep 30, 2020

- Sales of the company was up by 2% to Rs 1654.25 crore .

- Operating profit was up by 23% to Rs 382.69 crore.

- Other income increased by 6% to Rs 21.16 crore.

- PBIDT was up by 22% to Rs 403.85 crore.

- PBT was up by 67% to Rs 236.06 crore.

- PAT was up by sharp 89% to Rs 166.62 crore.

For the half year ended Sep 30, 2020

- Sales was lower by 18% to Rs 2876.22 crore.

- OPM expand by 160 bps to 21.4%

- Operating profit was up by 12% to Rs 615.81 crore.

- Other income stand higher by 9% to Rs 40.20 crore.

- However PBT was down by 11% to Rs 320.58 crore.

- PAT was up by 1% to Rs 232.39 crore.

Birla Corporation has reduced its debt from Rs 4172.77 crore a year earlier to Rs 4,060.65 crore at the end of September 2020 and that is despite spending close to Rs 800 crore on the upcoming factory at Mukutban over the past 12 months.

- Compounded Sales Growth of company has been 17% over 3 and 5 year period.

- Compounded Profit Growth of company has been 45% and 32% over 3 & 5 year period.

- Company has steady Operating profit margin of above 15% and Return on Capital Employed of about 7%.

- Company has cash and equivalents of about 256Crs sufficient to cater its short and long term needs.

Birla Corporation’s consolidated cost of borrowing is at 8.15%, down 168 basis points from a year earlier. Decreasing Interest rates are huge beneficiary for the company.

Outlook

In the recent budget as announced for physical infrastructure spending , it is targeted to be significantly higher in FY22 compared with previous years.

The recovery in cement demand would be sustained through the rest of the financial year, with various indicators pointing towards revival in the broader Indian economy. Real estate development in large metros, however, is still to pick up, so some uncertainties remain.

The strong rural demand that led to strong demand recovery in Q2FY21 is expected to sustain considering housing shortage especially pucca house in the key market of the company as well as expected strong rural income on the back of good agricultural crop.

Strong recovery in demand and ability to better price on the back of strong brands the company is expected to continue the growth momentum of Q2FY21 for rest of the fiscal.

The company is also investing in cement and clinker capacity addressing capacity constraints to support the growth as well as captive power capacity to control power & fuel cost. Overall, better regional presence, increasing share of premium cements share in overall trade as well as higher blending ratios, focus on cost rationalization and modernization will result in sustained improvement in BCL’s earnings going forward.

Conclusion-:

With significant expansion under progress and thrust from the government to increase its capex spending and revive infrastructure sector with a ton of initiatives announced in the recent budget Birla corp is worth exploring for long term. Increased rural demand for housing as well as significant increase in demand from tier 2 and 3 cities will add more via increase in sales and profitability to the company.

Please note that above expressed are our own views. Users are requested to take their own decision regarding investments. No member of DARKHORSESTOCKS would be responsible for any loss.

What is the target of Birla corp & poly Medicare for 6 months to 1 years sir please suggest

Sorry we dont provide target price.

what is the stock code of Birla Corp

It goes by the name birla corporation only.

Sir i would like to known your view on DCB BANK and Federal bank. Looks both are fundamentally good. Can u suggest the fundamentally good out of the two considering other factors. Can u tell us the factors to look into while selecting a good bank valuation wise.

Sorry we dont track any of these stocks.

Sir affle India future prospects

Sorry we dont follow that stock. Cannot help you with that.