India Nippon Electricals is a completely debt free 37 years old company , part of Chennai based TVS Group , a joint venture between Lucas Indian Service Limited, a wholly-owned subsidiary of Lucas-TVS Limited and MAHLE Electric Drives Japan Corporation, Japan – a company of MAHLE Group, Germany, engaged in manufacturing Electronic Ignition Systems for two-wheelers, three wheelers and portable engines.

1984 – Incorporation of Company

1987 – Supply to Bajaj Auto for Motorcycles.

1988 – Supply to Hero Motors – Moped.

1990 – Supply to Birla Yamaha (Now Birla Power Solutions)-Genset.

1995 – Supply to Mahindra Two Wheelers (formerly Kinetic Honda Ltd.) for Scooters.

1997 – Supply to Royal Enfield Motors Ltd.

2003 – Introduction of CDI cum Flasher Unit for 4S Motorcycle. Supply to Lombardini India for their 422cc Engine Supply to Piaggio India for their 3W application

2004 – Supply to Greaves for their General Purpose Engine Commenced Exports to Lombardini Italy for Diesel Engines

2004 to 2011 – Commenced Exports to Modenas Malaysia , Tomos, Slovenia , Beldeyama / Ramzey , Turkey , Yanmar, Italy , Kohler USA , Novamark, Slovenia , Arpres, Turkey.

2014 – Entered into partnership with Athena, Italy for EFI.

JOIN FOR DARKHORSESTOCKS WHATSAPP UPDATES

Incorporated in 1984 it was in 1986 the company had entered into the joint venture as mentioned earlier. India Nippon Electricals Limited makes the entire range of 2/3 wheelers, digital and analog ignition products. Over the years the company has successfully demonstrated to the two wheeler industry its ability to adapt to the changing business and technological needs of customers in the areas of quality and customer service thereby enlarging its customer base and now supplying to most of the manufacturers of two-wheelers, three wheelers and gensets.

As of March 31, 2020, Lucas Indian Services (LISL) holds about 45.87% stake and MAHLE Group about 20.52%.

INEL’s product portfolio covers all custom-built ignition system parts for various applications be it two wheelers, three wheelers or portable engines, making it a world-class company offering Ignition System solutions to meet the whole range of OEM’s in the vehicle industry.

The Company has three manufacturing plants located at Hosur, Tamilnadu; Kariamanikkam, Puducherry and Rewari, Haryana.

Product Portfolio

- AC Generator

- Regulator & Rectifier Unit

- Ignition Coil

- Exhaust Gas Recirculation Controller

- Engine Controller Unit-EFI

- Auto Choke-General Purpose Engines

- Dual Output Ignition Coil

- Throttle Position Sensor

- PM Alternator

INEL has successfully migrated to BS6 Emission norms for all the applicable existing products and customers. The company has not only succeeded in meeting the new requirements of the customers but also provided new value add features in the products leading to customer delight.

INEL, as part of aligning its strategy with the future needs of market and customer, is actively progressing towards development of new products in the area of displays and clusters, Sensors, DC-DC converters, Controller for EV, ISG and other automotive and non-automotive applications. It is continuously focusing on increasing presence in segments/ products like Sensors, expanding product basket for after-market as well as increase in share of business from customers and product lines. Thus to say company is Actively focused on development of new products in line with market/customer demand.

The company as part of diversifying its client base beyond 2/3 wheelers, was able to bag order from new customers in the commercial vehicle segment in FY20.

Strong relationships

TVS Motors (TVSM) and Hero MotoCorp are the two major OEM customers for the company. TVSM being part of the TVS Group, is a related entity as TVS Iyengar & Sons is the ultimate holding company of INEL. TVSM accounts for over 62% of revenue of the company sales in FY20. Morover, HMCL has awarded 100% share of business from its Neemrana Plant in Rajasthan, that has capacity of about 750000 units to INEL.

Foray in EV SEGMENT

Electronic products for automobile holds much promise for the future as the vehicles are getting more automated electronically and more complexities are expected in future. In this area the company is working to enhance its capabilities and capacities. The company expects it will stand to gain by offering comprehensive solutions through controllers and sensors.

Development of products for electric vehicle and non-automotive segments and increased global presence for existing products will be key. The establishment of tech center in Hosur, which is expected to be operational by Q4 of 2020-21, is a step in that direction. The New R&D Centre will have state of the art facilities for Performance and Emission testing of two wheelers, three wheelers and general purpose engines.

Company is actively working on a product portfolio that can provide product and solutions to EV players. It is in active discussion with many EV players. It has also won some business also in the area however the details of the same are not available.

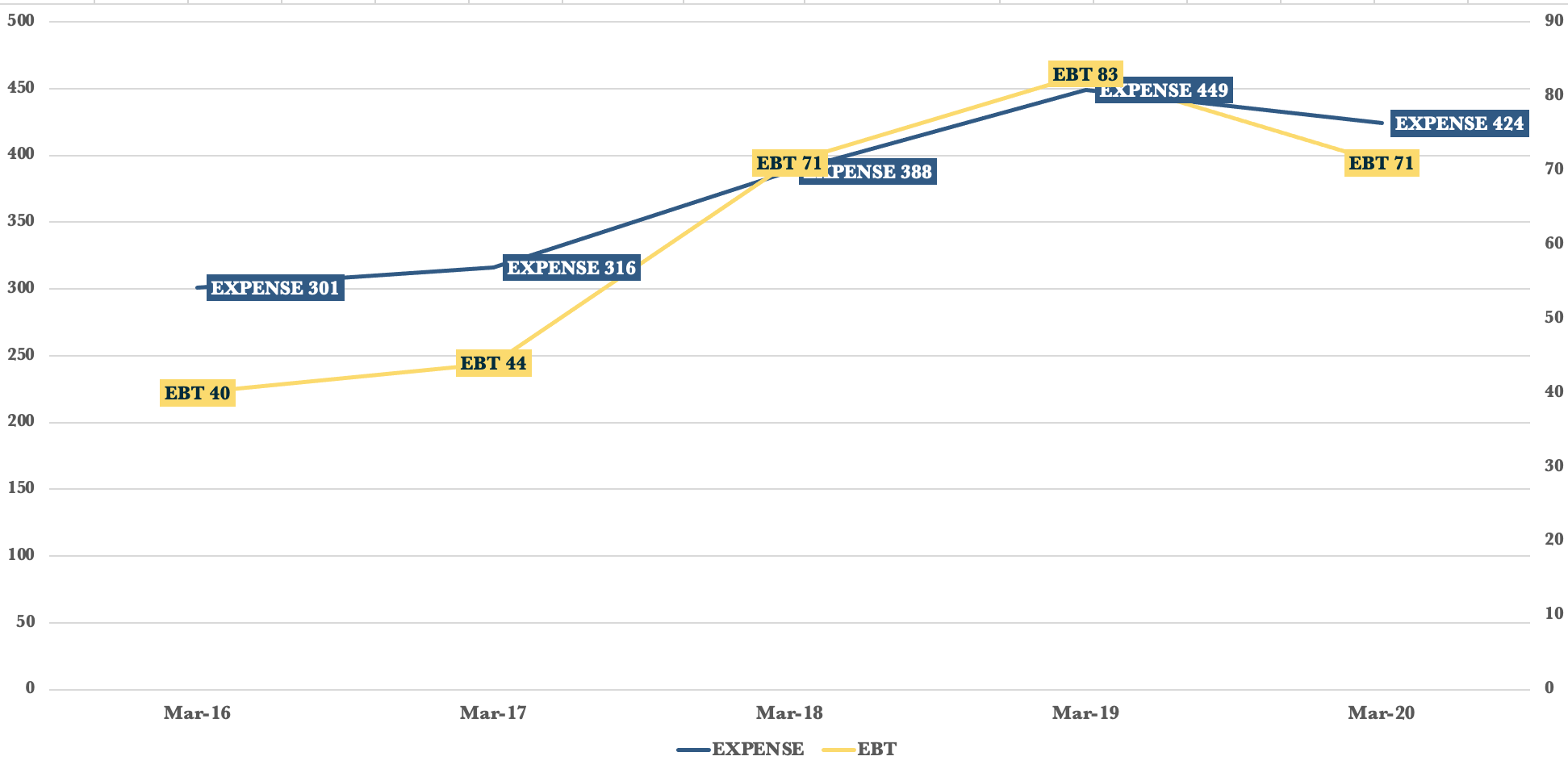

Financials

- Sales growth: for 10 years 13.42%

- Operating Profit: stable at 14% since FY2017-18

- Net Profit margin fluctuating between 11% to 7%

- Company has cash equivalents of 28 crores

- Investments of the company stands at around Rs 262 crores.

- Company is net debt free.

- 3 YEAR Profit cagr of company is around 21%.

Quarterly results for Dec 2020

- Net Sales at Rs 152.61 crore in December 2020 up 31.16% from Rs. 116.35 crore in December 2019.

- Quarterly Net Profit at Rs. 17.76 crore in December 2020 up 111.43% from Rs. 8.40 crore in December 2019.

- EBITDA stands at Rs. 23.55 crore in December 2020 up 62.98% from Rs. 14.45 crore in December 2019.

- India Nippon EPS has increased to Rs. 7.85 in December 2020 from Rs. 3.71 in December 2019.

Government Initiatives and Future Outlook

Post lockdown, need for social distancing and continued suspension/limitations of public transportation have triggered demand for personal mobility options where the two-wheelers along with passenger cars play crucial role. In personal mobility the preference is more towards two wheelers and next to passenger cars depending upon the affordability and traffic conditions in the urban centres of the country. Further rural demand which was largely unaffected with good agri income and expected good crop in coming season are boosting the demand for two wheelers.

Government pushing more for atmanirbar and lots of import duties on Chinese items. Going forward, there is a lot more interest from a lot of OEMs to localise many components Additionally company is planning on bringing in new products in terms of Tyre pressure monitoring sensor and also other controllers per se within the portfolio therein however details of any of those products have not yet been disclosed and management has said that the same will be disclosed in the AGM.

As the company’s major customers are two wheeler OEMs, the demand is expected to be strong on account of personal mobility requirement as well as festival demand in coming months especially from the second half of the current year.

Conclusion

India Nippon being a completely debt free company engaged in manufacturing OEE parts for 2 wheeler and 4 wheeler industry which is currently going a significant change in terms of preference and dynamics and additionally governments push for make in India initiative is also going to add fuel to the future growth to this sector and company in specific. Company is also on the path of foreign into the EV segment along with the new product launches which makes it very attractive bet. INEE peers trade at high P/E multiples given that India Nippon has good fundamentals, Market share and growth prospects if it is expected on a prudent basis that the sales of the company may grow around 10% from the pre covid levels for the Year ending march 2021 and slightest expansion in the earnings multiples can easily fetch 30%+ upside for the company in the coming period. However this is just an estimate which may or may not be true given that how the current covid situation turns out and what time it takes for the situation to normalise. Besides that India Nippon Electricals is good to explore for long term.

RPSG VENTURES

With a rich heritage of more than 40 Years, RPSG Ventures today is part of one of the most revered business conglomerates of India. With the group itself scaling new heights, with annual revenues of INR23,000cr and assets close to INR 41,000 Cr.; its extraordinary journey has just begun. RPG Ventures currently trades at around 300 rs while book value of the company is around 880 Rs. (Book Value- 880+ Rs)

Note-: Our work as compared to other is quite different. Unlike other blogs or others such service providers who provide research reports, share with a view to provide information or share articles mostly of well known companies which are known by all we specialise to bring it to the notice of users most unique and fundamentally strong companies which are know only to few people.

Good research done.