Bank of Baroda (BOB) is an Indian nationalised bank owned by the Government of India where it holds 64% shares. It is under the ownership of the Ministry of Finance of the government of India as well as the fourth largest nationalised bank in India, with 132 million customers having a global presence with more than 100 overseas offices.

Current Price-: 89 Rs

The bank was founded by the Maharaja of Baroda, Maharaja Sayajirao Gaekwad III in 1908. The bank, along with 13 other major commercial banks of India, was nationalised in 1969, by the Government of India and has been designated as a profit-making public sector undertaking (PSU).

In 1953 after Bank of Baroda opened its first overseas branch in Kenya and Uganda by establishing a branch each in Mombasa and Kampala. After that it opened anther branches is Nairobi , Tanzania at Dar-es-Salaam and today it has spread its operations across various cities such New York, London, Dubai, Hong Kong, Brussels and Singapore, as well as a number in other countries.

The bank is engaged in retail banking via the branches of subsidiaries in Botswana, Guyana, Kenya, Tanzania, and Uganda. The bank plans has recently upgraded its representative office in Australia to a branch and set up a joint venture commercial bank in Malaysia. It has a large presence in Mauritius with about nine branches spread out in the country. It is seeking approval for operations in Bahrain, South Africa, Kuwait, Mozambique, and Qatar, and is establishing offices in Canada, New Zealand, Sri Lanka, Bahrain, Saudi Arabia, and Russia.

Some of the key Subsidiaries of Bank of Baroda include

- BOB Capital Markets (BOBCAPS)-: It is a SEBI-registered investment banking company based in Mumbai, Maharashtra. It is a wholly owned subsidiary of Bank of Baroda. Its financial services portfolio includes initial public offerings, private placement of debts, corporate restructuring, business valuation, mergers and acquisition, project appraisal, loan syndication, institutional equity research, and brokerage.

- The Nainital Bank Ltd. (98.57%) was established in the year 1922 with the objective to cater banking needs of the people of the region. In the year 1973, Reserve Bank of India directed Bank of Baroda, to manage the affairs of the Nainital Bank Limited.

- BOB Financial Solutions Limited

- Baroda Asset Management India Limited (Formerly known as Baroda Pioneer Asset Management Company Limited) -: In 2008, Pioneer Global Asset Management SpA (“PGAM”) acquired 51% stake in the AMC, which was renamed as Baroda Pioneer Asset Management Company Ltd. and PGAM became a co-sponsor of the Mutual Fund. The joint venture had Rs. 30 crores in AAuM in June 2008 which grew to Rs. 12,044 crores in July 2019. The AMC continues its path of success as it grew to become a serious player in the mutual fund industry. In 2018, BOB acquired the entire shareholding of UniCredit S.p.A. (erstwhile PGAM, which merged into its holding company viz. UniCredit S.p.A. effective November 1, 2017) held in the AMC and Baroda Pioneer Trustee Company Private Limited (“Trustee”). Subsequently, the names of the AMC and Trustee have been changed to Baroda Asset Management India Limited and Baroda Trustee India Private Limited respectively, and the name of Mutual Fund has been changed to Baroda Mutual Fund.

- India First life Insurance Company Limited (44%)

- India Infradebt Limited (40.99%)

- Baroda Global Shared Services Ltd.

- Baroda UP Bank

Overseas Subsidiary

- Bank of Baroda (Botswana) Ltd.

- Bank of Baroda (Kenya) Ltd.

- Bank of Baroda (Uganda) Ltd.

- Bank of Baroda (Guyana) Inc.

- Bank of Baroda (New Zealand) Ltd.

- Bank of Baroda (Tanzania) Ltd.

- Bank of Baroda (UK) Ltd.

Overseas Associate

- India International Bank Malaysia Berhad

- Indo-Zambia Bank Ltd. (Lusaka)

Financials of the Subsidiaries

As ample amount of information is available about the establishment as well as the history of the bank we are not writing about it in more detail. Instead we are focussing on the difficult part which is to bring more information about the business of the company.

Appointment of Hasmukh Adhia as Non executive Chairman

Hasmukh Adhia, IAS is a Former Finance Secretary and Revenue Secretary. He is one of the key persons behind the architecture and roll-out of the Goods and Services Tax & Demonetization scheme announced in 2016. In 2019 GOI appointed former Finance Secretary Hasmukh Adhia as chairman of state-owned Bank of Baroda (BoB).

Mergers

The bank has completed its integration with the former Dena and Vijaya Bank. During the year, the Bank combined or rationalised 1,310 branches and 1,135 ATMs as part of the integration. At the same time, as of March 31, 2021, the Bank’s Business Correspondent (BC) network had grown by 5,200 to 23,320. In PMJDY deposits, the Bank has a 16.24 percent market share. The Bank intends to have 50,000 contact points in the next two years, including BCs and other forms (mini branches and service outlets). To provide seamless customer service across the country, these touch points would be new-age, compact, and digital. This will aid the Bank in expanding its branch network in underserved areas. Customers will now have access to 8,248 domestic branches and 10,318 ATMs throughout the country.

Business Details

Accounts

Bank of Baroda offers different type of accounts to meet your financial goals and secure your future. Choose from our wide range of deposit products that are specifically designed to keep your unique requirements in mind.

Loans

Bank of Baroda offers a wide range of loans to meet your diverse needs. Whether the need is for a house, child’s education, our unique and need specific loans will enable you to convert your dreams to realities.

Investments

Bank of Baroda offers various investment products suited to cater varied investor profiles.

Insurance

Through tie-ups, BOB have made available a bouquet of insurance products to meet the financial and investment needs of customers. It also offers various tailor made Wealth Management Products.

Digital Products & Merchant Payment Solutions

Bank of Baroda provides various digital products like ATM, debit card, mobile banking, internet banking, etc. to make banking experience smooth and save time & money. These products help customer in banking without actually walking into the branch.

Other Services

Apart from the Loans, Deposits and Cards, Bank of Baroda offers other services such as capital market services, collection services, ECS, etc.

Focus on Digital Banking

The Bank of Baroda is adjusting to the changing environment by launching the Smartphone First Bank mobile application, which will serve as the principal interaction with clients. The bank has updated its mobile app and added new features so that consumers don’t have to visit a branch unless it’s absolutely necessary. Small-ticket personal loans have already been digitised, and the remaining sectors will be migrated to this platform over time.

In the loan industry, the Bank is also digitising client journeys. The goal is to digitise the whole loan process in the retail and MSME sectors, from sourcing to sanctioning to payout.

Newest Initiatives taken by the bank

The Bank opened 1.24 crore new CASA accounts during the year. The focus was on using tablets to open accounts in a paperless manner (TAB).

Baroda Defence Salary Package, a tailor-made salary account product for active and retired defence services personnel, was also launched by the bank.

Nearly 30,000 salary accounts were formed under the Baroda Government Employees’ Salary Account Scheme, with a total of Rs. 397 crore mobilised and an average balance of Rs. 1.41 lakh per account.

The platform’s connection with the Ministry of Corporate Affairs (MCA) site for online current account establishment of new firms established using the platform resulted in the Bank receiving over 7,000 current accounts with an average balance of Rs. 2.50 lakh.

In conjunction with TATA AIG, Max Bupa, and Star Health Insurance Company, the Bank launched SB account-linked insurance products and opened 1.73 lakh insurance-linked SB accounts in FY 2021.

Financials

For the year Ended March 2021

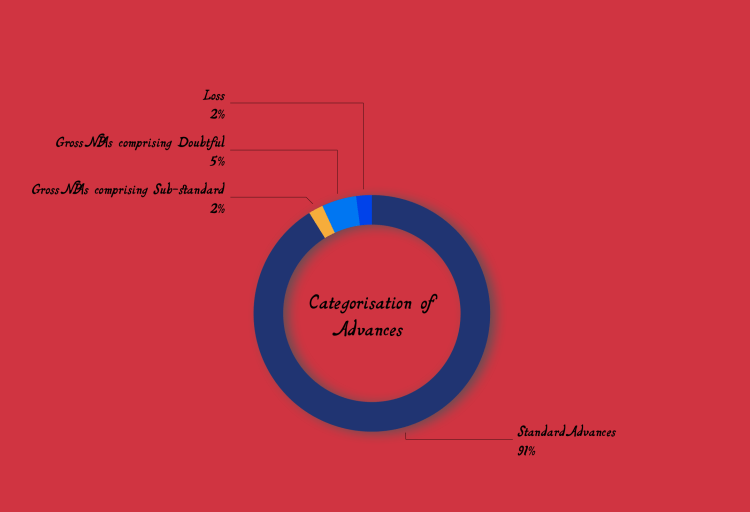

Despite the economic effect of the pandemic, the bank’s asset quality increased during the year ending March 2021. The Bank’s gross non-performing ratio fell to 8.87 percent as of March 31, 2021, down from 9.40 percent as of March 31, 2020. Domestic business credit cycle appears to be changing, as domestic credit cost fell to 1.54 percent in FY 2021 from 2.51 percent in the previous fiscal year. As of March 31, 2021, the Bank’s total provision coverage ratio remained unchanged at 81.80%.

Domestic CASA deposits at the Bank grew by 16.48 percent in FY 2021. The Bank’s current account deposits climbed by 24.09 percent, while savings deposits increased by 15.06 percent. As a result, the Bank’s CASA ratio grew by 380 basis points to 42.87 percent as of March 31, 2021, up from 39.07 percent as of March 31, 2020.

In FY 2021, the Bank’s domestic credit off-take grew at a rate of 5%, which was in line with industry growth. In addition, the Bank’s MSME, retail, and farm portfolios grew by double digits. A 32.64 percent rise in gold loans boosted the agriculture sector. Both secured and unsecured loans increased across the retail credit portfolio. In FY 2021, for example, the vehicle and personal loan books climbed by 27.79 percent and 27.21 percent, respectively.

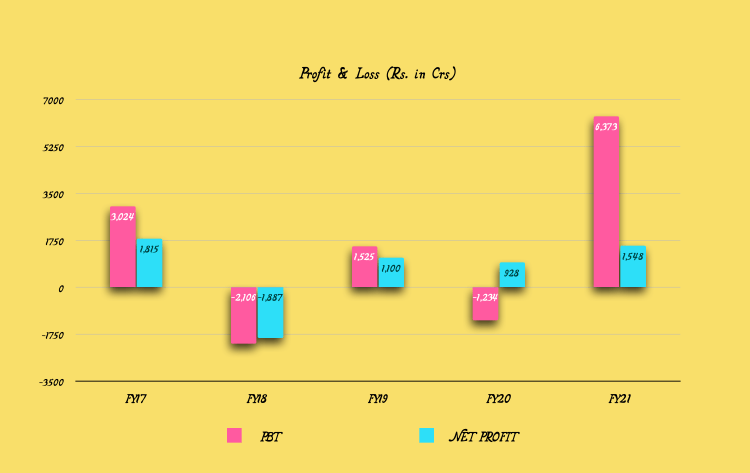

In FY 2021, the bank increased its operating profit by 9.17 percent to Rs. 20,630 crore.

The bank’s profit before tax grew to Rs. 5,556 crore in FY 2021, compared to a loss of Rs. 1,802 crore the previous year.

In FY 2021, the bank made a profit after tax of Rs. 829 crore, up from Rs. 546 crore in FY 2020. Bank’s profit after tax would have been Rs. 4,143 crore if the one-time impact of DTA had been taken into account.

The capital adequacy ratio (CRAR) of the Bank improved to 14.99 percent as of March 31, 2021, up from 13.30 percent as of March 31, 2020. Internal accrual of Rs. 4,143 crore, fresh equity issue of Rs. 4,500 crore, and AT-I bonds of Rs. 3,735 crore contributed to this. As a result, the Bank’s standalone CET-I ratio increased to 10.94 percent as of March 31, 2021, up from 9.44 percent as of March 31, 2020. As of March 31, 2021, the Bank’s CRAR was 15.74 percent and CET-I was 11.80 percent on a consolidated basis.

Credit Expansion

The bank’s outstanding net credit climbed to Rs. 7,06,301 crore as of March 31, 2021, with domestic advances totaling Rs. 6,05,616 crore. Retail, MSME, and agricultural led the surge in domestic advancements. Organic retail loans climbed to Rs. 1,20,256 crore, with vehicle and personal loans driving the growth. As a result, the retail loan to total domestic loan ratio grew to 20.68 percent throughout the year. As of March 31, 2021, the overseas loan book was at Rs. 1,00,685 crore.

Corporate Credit

Corporate credit is served by 15 Corporate Financial Services (CFS) locations, which manage about 73% of the Bank’s entire corporate credit portfolio. As of March 31, 2021, the Bank’s corporate credit portfolio has grown to Rs. 2,91,615 crore.

MSME Credit

The MSME portfolio stands at Rs. 96,200 crore as of March 31, 2021. In fiscal year 2021, the bank added 2.72 lakh new MSME clients. The bank expanded its dedicated SME processing centre network from 27 to 71 SME Loan Factories (SMELF). Furthermore, 15 additional SME branches were created to provide consumers as a one-stop solution for all financial needs, including personal loans, deposits, forex-related services, and financial solutions for promoters.

As of March 31, 2021, the bank’s mortgage-based loan book (home, mortgage, and rent receivables) was at Rs. 99,630 crore.

Personal, housing, and school loans increased by 27.21 percent, 11.10 percent, and 9.06 percent, respectively, within the retail industry.

Auto loans climbed by 27.79 percent for the bank, compared to 9.50 percent for the sector.

As of March 31, 2021, the bank had opened 27 new Specialised Mortgage Stores (SMS), for a total of 126 SMSs. These locations are spread around the country in order to provide specialised and speedier mortgage-based retail credit delivery.

In-principle approval for retail loan products such as house loans, personal loans, and vehicle loans is now done online using the Digital Lending platform. Customers with liability can apply for end-to-end online micro personal loans of up to Rs. 50,000 from the bank.

Rural and Agricultural Lending

The bank has a network of 2,852 rural branches and 2,090 semi-urban branches that are used for priority sector and farm loans. Agriculture advances from the bank climbed to Rs. 99,543 crore as of March 31, 2021.

Priority Sector Lending

The bank’s priority sector advances increased by 10.14 percent during FY 2021, from Rs. 2,26,336 crore on March 31, 2020 to Rs. 2,49,285 crore on March 31, 2021. As of March 31, 2021, the bank had met all of the necessary objectives for Priority Sector Lending segments.

Gold Loans

The bank’s gold loan portfolio climbed by 35.64 percent to Rs. 23,593 crore as of March 31, 2021, up from Rs. 17,393 crore the previous year. Agriculture gold loans increased by 32.64 percent in FY 2021 to Rs. 22,492 crore. Retail gold loans increased from Rs. 436 crore on March 31, 2020 to Rs. 1,101 crore on March 31, 2021. Gold Loan Shoppes led the way, increasing from 185 to 984 within the same time period.

The proportion of gold loans in agricultural loans climbed from 19.13 percent in fiscal year 2020 to 22.30 percent in fiscal year 2021. The average size of a gold loan ticket grew from Rs. 1.05 lakh to Rs. 1.36 lakh.

Other Highlights

- Basic Saving Bank Deposit (BSBD) accounts increased by 78.13 lakh (15.26%) and deposits increased by Rs. 4,791 crore (25.58%).

- Pradhan Mantri Jan Dhan Yojana (PMJDY) accounts increased by 83.34 lakh (20.30%) and PMJDY deposits increased by Rs. 4,340 crore (30.36%).

NPA

Financials for Q2FY22

- On a year-over-year basis, NII was unchanged at 7566 crore, down 4.1 percent QoQ, owing to a 19 basis point drop in NIMs to 2.85 percent. Other revenue increased by 25% quarter-on-quarter and 27.7% year-on-year to 3579 crore.

- The bank has charged 145.4 crore in extra pension-related charges and has a balance of 1308.9 crore carried forward. Provisions fell 31.3 percent year over year to 2754 crore. As a result of the decreased provisions, PAT increased by 24.4 percent year on year to 2088 crore.

- Asset quality was constant, with GNPA and NNPA down 75 bps and 20 bps QoQ, respectively, to 8.11 percent and 2.83 percent, while restructuring remained mostly unchanged at 3 percent vs. 2.9 percent QoQ. Slippages during the quarter totaled 5802 crore, owing to the loss of one significant account.

- Domestic loans increased by 2.99% year on year to 6.2 lakh crore. Sequential increase, on the other hand, was decent at 3.8 percent. Retail loans increased by 10.2 percent year over year, while agri loans increased by 7.3 percent year over year. Deposit growth remained steady at 0.5 percent year over year at 9.5 lakh crore, with CASA deposits growing 13.01 percent year over year.

Management Comments

- Home loan growth has been slow, but it is expected to rise up in the future.

- The use of working capacity is expected to increase. However, it will take a few more quarters for Capex to catch up.

- A stressed NBFC exposure of 2000 crore was categorised as a nonperforming asset (NPA) and 50 percent provisions were imposed on it.

- In H2FY22, management anticipates recoveries of 7000-8000 crores, with loan book growth similar to the industry average.

- Large corporations account for 7400 crores, MSME for 6700 crores, and retail for 5400 crores of the overall restructuring. For FY22E, a 2% slippage rate is expected.

- Bank of Baroda has enjoyed a considerable amount of revenue from treasury operations over the previous two quarters, but since interest rates have begun to tighten, treasury income will moderate moving forward.

- The bank has provided 50% of the exposure to SREI Infra, which is worth INR20 billion.

- Although it may take time for credit growth to recover due to the strengthening credit cycle, management appears to be quite optimistic about upcoming H2FY22 as well as the for the coming years.

CONCLUSION

Bank of Baroda is a Government Owned Public Sector Undertaking and after the amalgamation of Vijay Bank and Dena Bank with Bob it is now one of the biggest Nationalised Bank in the country. Over the past several quarters bank had struggled largely with Increasing NPA, write-off as well as for some of the quarters it has posted losses consistently. However for the current quarter it posted highest net profit ever and it is expected that the bank is on further path of profitability with the worst behind. Additionally there is immense business potential within the Bank’s customer base. For instance, the Bank can grow its corporate business wallet share by offering full-service solutions, with initiatives to holistically understand customer needs and offer the entire gamut of financial products. The wealth management business too has immense potential within the Bank given the large base of MSME and high net worth clients. The Bank is overhauling its wealth business to enhance its value proposition. With the Government backing and highly qualified top management it is completely wise to expect that Bank of Baroda can surely be on a path of turnaround. Thus this makes BOB worth exploring.

Note-: Our work as compared to other is quite different. Unlike other blogs or others such service providers who provide research reports with a view to provide information or share articles mostly of well known companies, we specialise to bring it to the notice of users most unique and fundamentally strong companies.

One thought on “Financial Resilience: Profiling a Government-Owned Bank’s Performance Amidst Challenges”