AU Small Finance Bank Limited (AU Bank) is a commercial bank, a Fortune India 500 company, and the country’s largest Small Finance Bank based in Jaipur, India. Q4 FY’22 marks the completion of its 20-quarters of banking operations and so far it had a stellar record which is expected to continue in the coming period as well.

(AU Small finance bank was previously suggested on 19th April 2020 when the stock was trading at 540 Rs (Without Bonus/270 Ex bonus) and since then it has delivered 170% returns before falling to current price.)

AU SMALL FINANCE BANK

Current Market price on the date of publishing this report-: 614 Rs

AU Bank began its journey in the Rajasthan hinterlands and has grown to become the leading Small Finance Bank with a profound grasp of rural and semi-urban areas, allowing it to establish a sustainable business strategy that facilitates equitable growth. It was started in 1996 as AU Financiers (India) Ltd as a car finance firm and changed to a small finance bank on April 19, 2017. AU Small Finance Bank provides poor and middle-income individuals, as well as micro and small firms, with little or no access to mainstream banking and finance channels. The bank provides loans, deposits, as well as payment goods and services.

Bank opened 39 new touchpoints taking its network is spread across 919 touchpoints

From lending to 5.6 lakh consumers in 2017 to serving 27.5 lakh customers presently, AU SFB has grown to tremendously. Today it has 919 touch points across 18 states and 2 UTs as of 2022. It has expanded from an 8,500-person family to a winning team of 27,800+.

The total growth of the AU Bank over 5 years can be seen from the table below

AU Sfb has recently ventured AU 0101 Credit Cards/QR Code/Video Banking and many other things thereby expanding its presence across all the products, AU Sfb also plans to increase its presence in Housing Loans where it has very little exposure.

AU SFB has divided itself across five SBUs — Digital Banking, Credit Card, Merchant Solution Group, Wheels and Home Loan. Bank has provided with detailed business strategy and outlook for two of these products and for the remaining products it should be out soon.

Business products and other things are not very relevant since ample, clear and precise information about the same can be found from the company website. Therefore in order to save your time we are not getting much into products by showing you with unnecessary images and descriptions of the same.

Financials

NPA

NPA came below 2% at 1.98% and net NPA reducing to 0.5%

Gross NPA fell by 62 basis points from 2.6 percent in Q3 to 1.98 percent in Q4. Absolute value decreased by Rs.133 crores from Rs.1,058 crores in Q3 to Rs.924 crores in Q4.

Net NPA fell from 1.3 percent in the third quarter to 0.5 percent in the fourth quarter. There was a gross reduction of Rs.329 crores in Q4 from the Q3 closing NPA of Rs.1,058 crores, resulting in 31 percent resolution during the quarter, with 65 percent resolution occurring through normal question efforts and approximately 28 percent resolution occurring through security enforcement, with a POS loss of approximately 38 percent.

Another 7% of the resolution was due to a technical write-off.

Wheels Business

Wheels business financed 85,000+ automobiles during Q4 FY’22, equating to a total disbursement of Rs.3,667 crores, representing a 25% year-on-year and 20% quarter-on-quarter basis.

Wheels’ total AUM is currently Rs.17,300 crores, with an average ticket size of Rs.3 lakhs. At the AUM level, 60% of financing is for new automobiles, 38% is for used and refinancing, and 2% is for two wheelers. Light commercial vehicles and passenger vehicles have shown more demand than other sectors.

SBL Business

With Q4 FY’22, demand in the SBL business is gradually returning. The Disbursement is equal to the same quarter last year at Rs.2,116 crores. Total AUM of SBL company has now reached Rs.16,524 crores across 2 lakh MSMEs, representing a 15% year-on-year increase.

Housing Loans

The housing financing sector showed high demand in Q4, with a total disbursement of Rs.673 crores, a 54 percent increase year on year. The total AUM of the housing company is currently Rs.2,654 crores, spread across 27,000 dwelling units, representing a 19% increase year on year.

Commercial Banking Business

Commercial banking industries such as business banking and agri banking continue to thrive and establish themselves in the market. These are both granular enterprises.

In Q4 FY’22, commercial banking disbursed Rs.2,529 crores, a 104 percent increase year on year, with the majority of enterprises eligible for low-cost refinancing.

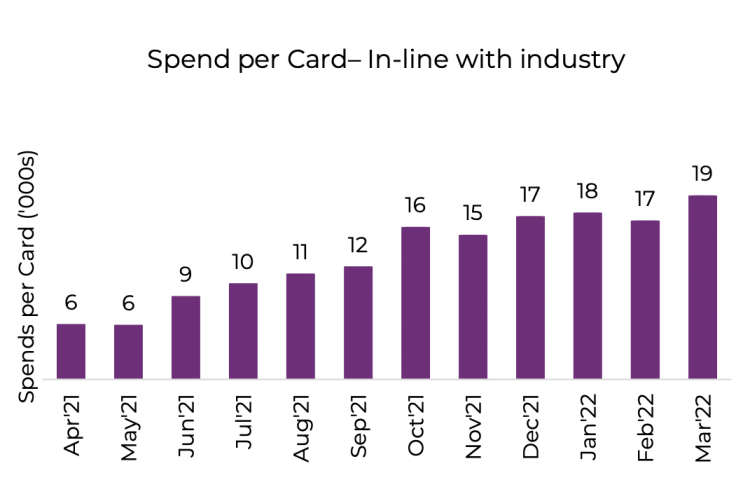

Additional initiatives have had positive results, with over 40% of additional clients acquired to the bank in Q4 via AU 0101, video banking, credit cards, and UPI QR codes.

Company has so far issued 1.7 Lac+ with a Monthly run rate of ~25,000 cards of which 49% are first time credit card users and average limit of all the cards issued is 1.1 lakh Rs.

General Banking

Clients with saving accounts are 64 percent more likely to use AU 0101 app, while current account customers are 77 percent more likely to use internet and mobile banking. In addition, in Q4, 1.9 lakh unique AU debit card holders transacted. Debit card transaction volume surged dramatically in March ’22, surpassing 4 lakh transactions, and spending has regularly been in the Rs.100-plus crore range in the previous three months. The average product per client has risen to 1.7 for Savings account customers and 1.9 for Current account customers. Two or more Au SFB’s products are used by 62 percent of current account clients and 47 percent of savings account customers.

AU Bank now has 184 urban branches, with 64 of them opening in FY22. Sixteen of these new branches, with a six-month average vintage, have already increased their deposits to Rs.50-100 crores.

This quarter, mutual fund AUM surpassed Rs.100 crores, and AU Bank has close to 60,000 – 3 IN 1 trading accounts through its cooperation with Motilal Oswal Financial Services.

Business

- The bank’s overall balance sheet increased by 34% year on year to 69,078 crore.

- Deposits increased by 46 percent year on year to 52,585 Cr, with CASA at 37 percent, up from 23 percent on March 31, 2019.

- The cost of funds fell by 88 basis points year on year to 5.9 percent.

- Loan AUM increased by 27% year on year to 47,831 Cr, with a CD ratio of 88%.

- The retail loan book accounts for 88% of the loan book.

Profitability

- Total income was 6,915 crore, up 21% year on year; NII was 3,234 crore, up 37% year on year.

- The net profit for the fiscal year FY22 was Rs. 1,130 crore.

- ROA was 1.9 percent, and ROE was 16.4 percent.

Deposits

General Operations

The bank’s total advances increased by 32% year on year to 46,789 crore from 35,356 crore. This was accompanied by steady collection efficiency in excess of 100% for each month of the quarter, resulting in persistent improvement in asset quality ratios.

Deposits increased 46 percent year on year to 52,585 crore from 35,979 crore, with the CASA ratio improving to 37 percent from 23 percent a year before. The overall business environment’s continued development resulted in robust disbursements. Fund-based payments increased 39 percent year on year in Q4FY22, reaching Rs 10,295 crore from Rs 7,421 crore in the same period the previous year. In Q4FY22, disbursements included ECLGS of 64 Crore.

Non-fund disbursements in Q4FY22 increased by 90% year on year to 742 crore, compared to 391 crore in the same period the previous year.

Current Account Customers

Currently, around 50% of clients have an asset relationship, but AU SFB is dramatically increasing this number. It also has a huge rural base, so 62 percent of QR are active, and 90 percent of those QR customers have an account with AU SFB, which flows into the bank account and improves the bank’s CA balances significantly.

So, going forward, the bank is clearly looking at manufacturing and services customers separately from merchant segment customers, as merchant segment customers are where AU has a very strong franchise and capability, and where the bank is building digital lending capabilities as well as QR and cost-related payment solutions. And there is where management believes their volumes will considerably increase, given more than 80% of its CA book is now sole proprietors and small firms.

Asset Quality and Capital Adequacy Ratio

- Provision coverage ratio is 75 percent, up from 50 percent on March 31, 2019. Collection efficiency averaged 106 percent for the fiscal year FY22.

- Aside from the 653 crore provision against the GNPA pool, the bank has also maintained the provision buffers listed below.

- 192 crore provision against restructured book (16 percent of restructured book)

- A 157 crore contingency provision (0.34 percent of advances)

- 41 crore floating provision (0.09 percent of advances)

- 139 crore standard provisions (0.30 percent of advances)

- The bank is nonetheless adequately capitalized, with a total CRAR of 21.0 percent versus the minimal requirement of 15 percent.

- Tier-I capital ratio of 19.7% versus the minimal requirement of 7.5 percent

The bank’s perspective on the influence of interest rates on the NIM in the next quarters is as follows:

The bank’s cost of funds starts around 5.6 percent, and last year it had a cost of funds on an overall basis of 5.9 percent. So it still has some leeway to manage even if the cost cycle rises by 50 or 75 basis points. Furthermore, the bank has the capacity to pass this cost on to its customers because they are not rate sensitive, and it has cut rates through the years. As a result, the type of consumer with whom AU SFB works is a core market. And if the interest cycle rises, so will the entire NBFC and that segment. So management strongly believes that they can protect their NIMs as they move forward in the range bound interest rate cycle upwards.

Conclusion

AU Small Finance Bank Limited (AU Bank) is a commercial bank, a Fortune India 500 company, and the country’s largest Small Finance Bank.

With a 27-year legacy of being a retail-focused and customer-centric institution, AU began banking operations in April 2017 and as of March 31, 2022, it had established operations across 919 banking touchpoints while serving 27.5 lakh customers in 18 states and two union territories with a workforce of 27,817 employees. The bank has a net value of 7,514 billion rupees, a deposit base of 52,585 billion rupees, and assets under management (AUM) of 47,831 billion rupees. AU Bank is trusted by prominent investors and is listed on both the NSE and the BSE. All major rating agencies, including CRISIL, CARE Ratings, and India Ratings, have regularly assigned it a strong external credit grade.